Financial lessons we’ve learned from the pandemic

Daniel Coughlin

27 October 2020

What COVID-19 has taught us about money management

The coronavirus crisis has upended our lives in ways we could never have imagined. But among the silver linings to be gleaned from the pandemic, apart from the obvious such as spending more time with immediate family, are the money management lessons COVID-19 has taught us. From the importance of building up an emergency fund to diversifying investments and developing a lucrative side hustle, click or scroll through 30 sound financial lessons we've picked up due to the pandemic.

Relying too much on a 'stable' income is shortsighted

If there's one thing this pandemic has taught us, it's that no job is 100% secure, however safe it may seem. The crisis has also shown that revenue from myriad types of investments can drop suddenly and even dry up completely because of circumstances beyond our control. For these reasons, relying too much on a 'stable' income can leave you vulnerable financially.

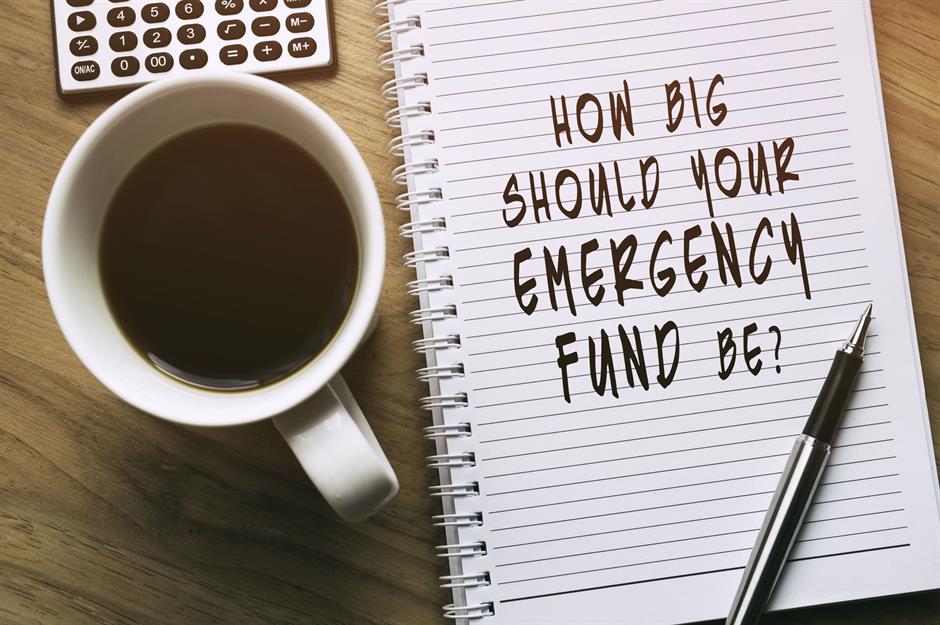

Building up an emergency fund is a must

The pandemic has confirmed what those who are sensible with their money have known for a long time: an emergency fund to cushion you from the shock of a crisis is essential. These savvy financial operators have a rainy-day sum of money squirrelled away in a separate high-yield savings account that they can dip into when the need arises.

Setting aside enough to tide you over is crucial

Having an adequate amount of money to see you through a crisis is of course the whole point of a contingency fund, but even a relatively small sum of cash will help. Ideally, the US Federal Reserve and UK Money Advice Service recommend you set aside enough to cover three months' essential outgoings, while some financial experts suggest you should aim to cover six months'-worth.

Budgeting in a crisis can make all the difference

Knowing exactly how much cash is coming in and going out is doubly important during a crisis when money might be tight. A simple spreadsheet will work, but downloading a budgeting app such as Mint, BudgetTracker, Wally or PocketGuard, or using an online money management tool like BudgetTracker could make the process even easier.

Putting your money into the stock market can be seriously risky

The longest bull market in history may have lulled some investors into a false sense of security and given them the impression their stock portfolio would go on rising in value indefinitely. The coronavirus-induced crash in March served as a painful reminder that the market is a volatile creature, stocks can go down in price as well as up and investments are risky endeavours.

Investing is for the long term

Be that as it may, the stock market has more or less recovered since the sharp COVID-19 dip in March. The key takeaway from this is that stocks are long-term investments, not short-term money generators. It's all about being patient and potentially holding onto shares when the chips are down because they could recover in value in the future.

Diversifying your investment portfolio is essential

The pandemic has reminded us not to put all our investment eggs in one basket. In fact, the best hedge against stock market volatility is a diverse portfolio that spreads the risk. If the bulk of your investments are in airlines for instance, COVID-19 will have no doubt slashed the value of your portfolio. If however you'd diversified with some pharmaceutical stocks, your losses would have been offset very nicely indeed.

Paying off credit card debt is a smart move

The last thing you need in a crisis is a massive credit card debt hanging over your head, especially if the rate of interest is sky-high, as is all too often the case. Some providers have been offering credit limit increases, payment holidays and other coronavirus relief measures but few are freezing interest for hard-up customers and any assistance is temporary.

Clearing other high-interest debt should also be a priority

As the pandemic has made crystal clear, settling other high-interest debt like loans should also be a priority. Again, while some lenders have been willing to help struggling customers by offering them payment holidays and waiving missed payment charges, the relief measures won't last forever and sooner or later the debt will have to be paid off.

Finding a better credit card deal and consolidating other debt is sensible

If you can't clear your credit card or other high-interest debt, shopping around for an interest-free or cheaper deal is the way forward. Hitting the price comparison engines and finding more affordable alternatives can save you a significant amount of money, which is music to anyone's ears during these challenging times.

Avoiding taking on any new debt is prudent during a crisis

Interest rates may have plunged to historic lows, but this pandemic has also taught us that taking on new debt in the middle of a crisis is fraught with risk. Signing up for a credit card or loan and saddling yourself with additional debt is not the best of ideas when job insecurity is so rife and the economic outlook so uncertain.

Now read: The biggest economic bubbles of all time

Cutting back on luxuries isn't actually that difficult to do

Through lockdowns and social distancing measures, COVID-19 has forced us to embrace a simpler life and go back to basics. For some people, forgoing expensive dinners in their favourite restaurant or going without designer clothing and other fancy things they don't need has actually been a freeing experience and not half as hard as they might have thought.

The temptation to splurge online can be hard to resist though in a pandemic

For others, the temptation to splurge online can be hard to resist when they're stuck at home so much. As well as panic buying, so-called 'comfort buying', online retail therapy triggered by anxiety, has surged during the pandemic as people look for ways to ease their coronavirus-induced stress.

Splashing out on a daily coffee and lunch drains your finances

It has taken a pandemic and mass homeworking for many people to realise that splashing out on a barista-made coffee and buying lunch every day is a big drain on their finances. They've cottoned on to the fact that they can save thousands a year by packing their lunch and skipping the shop-bought morning coffee.

Working from home can save you a fortune

Indeed, working from home has been something of a windfall for anyone lucky enough to be able to do it with many former commuters saving a fortune on travel expenses. And the money they've saved on a travel card, rail season ticket or petrol, along with the daily coffees and lunch more than offsets any remote working costs such as pricier utility bills.

Now read: How COVID-19 could change cities forever

Claiming tax deductions if you work from home is a thing

Many office workers may not have been aware before the pandemic hit that they can claim tax relief on their job expenses when they work from home. Examples of allowed expenses include heating, water and broadband costs, and remote employees can even offset their tax bill by claiming on any work-related equipment they buy such as a laptop or office chair.

Making rash financial decisions is rarely clever

The pandemic has driven some people to make rash financial decisions. From panic buying and stocking up on unnecessary items to cashing in long-term investments when the market dipped only for it to recover mere months down the line, many people may regret actions they took at the start of the pandemic. Crisis management calls for a cool head and decisions made in haste are rarely clever ones.

Using the internet for free financial advice and money management tools can be enlightening

People have had more spare time to go online as a result of the pandemic and with remote learning booming, many have been using this time judiciously to boost their financial literacy. The internet is awash with sites offering free financial advice, not to mention money management tools and other useful resources, which have come into their own during the crisis.

Knowing what you're entitled to is super-important

Knowing exactly what you're entitled to is vital, because often you will have to request support rather than automatically receive it. Whether it's a tax, credit card or mortgage payment holiday, flight refund, self-employed grant or any of the numerous other types of relief offered by the government and private sector, read any information your bank or service providers send you and follow the news and look at government websites to stay on top of the latest financial support offerings and get in touch with them if you think you qualify.

Communicating with organisations you owe money to is always advisable

Even if financial organisations aren't actively advertising support packages, it is a good idea to let them know if you need help. The pandemic has shown that being proactive and communicating with any lenders, service providers and tax authorities is always advisable if you're experiencing financial difficulties. Burying your head in the sand won't make things better while facing the music and reaching out will ensure you get the assistance you need.

Investing in buy-to-let properties comes with major risk

COVID-19 has brought to light the danger of depending on buy-to-let income. A recent survey by market research firm YouGov found that almost a quarter of private landlords in the UK have seen a reduction in their rental income as a consequence of the pandemic as hard-up tenants, who were protected from being evicted for a number of months, stop payments or negotiate rent reductions. The crisis has also highlighted the importance of obtaining rent guarantee insurance.

Developing a lucrative side hustle makes good financial sense

The pandemic is also showing us that developing a lucrative side hustle makes good financial sense. With so many jobs on the line, having something you can fall back on can help you keep your head above water. This could be anything from taking a part-time job delivering groceries or takeaway food to a sideline selling homemade masks or hand sanitiser on Etsy.

Now read: Super successful companies that started as a side hustle

Creating multiple income streams is even better

Having multiple revenue streams you can tap into is even better as this crisis is proving. That way, you're insulated to the max from a financial meltdown. Think about your skills, work out what you'd be good at and be prepared to multitask and jump from one money-making side gig to the other.

Taking out income protection insurance gives you peace of mind

Insurance was invented for times like these and the pandemic has punctuated the need for comprehensive coverage to enable you to keep paying the bills if you fall ill or lose your job – after all, government assistance only goes so far. Income protection insurance, though costly, is therefore one of the best ways you can protect your finances from the worst that can happen.

Signing up for a mortgage protection insurance policy is the next best thing

If income protection insurance is beyond your budget but you still want to prevent your home from being repossessed should you be made redundant or get seriously ill, mortgage protection insurance is the next best thing. While not as comprehensive as income protection insurance it will cover your mortgage repayments for a certain period of time, and tends to be cheaper.

Travelling without insurance is foolish

COVID-19 has resulted in countless cancellations of flights, hotel bookings and other travel plans, and while regulations state airlines, hotels and travel companies must issue refunds, many people have struggled to get their money back. This makes travelling without insurance that covers against cancellations all the more foolish.

Taking out a life cover policy shouldn't be put off

Life insurance sales have been surging due to the pandemic, particularly in the US where people are reportedly panic buying policies. Taking out life cover isn't something anyone enjoys doing but ensuring you provide for your loved ones in the event of you passing away is a responsible thing to do, especially if they rely on you financially.

Getting your estate in order is morbid but necessary

Staying with morbid financial lessons, COVID-19 has stressed the importance of getting your affairs in order. As with taking out a life insurance policy, drawing up a last will and testament is something many people would rather avoid doing as nobody likes being reminded of their mortality. Nonetheless, failing to write a will can cause serious problems for the people you leave behind.

Watching out for scammers and fraudsters is vital during a pandemic

Ever eager to exploit a crisis, scammers and fraudsters, both on and offline, have been keeping themselves very busy during the pandemic, using tactics including phishing emails and texts, robocalls, imposter schemes, and posing as government and tax officials to dupe their unsuspecting victims. It is more important than ever to watch out for any unsual communications from your service providers, and make sure that you never provide your financial details to anyone unless you are sure they are who they say they are.

Discover the online scammers' tricks to watch out for during the pandemic

Sitting down (remotely) with a financial advisor can save you money

Lastly, you can read all the money-saving articles in the world and wear out your budgeting apps and online tools, but nothing beats the sage advice of an independent financial advisor, who can offer you pointers tailored to your specific situation, helping you stay solvent through the pandemic and beyond.

Now discover the cost of cancelling 2020's mega-events

Comments

Be the first to comment

Do you want to comment on this article? You need to be signed in for this feature