Pension saving: mid-life women facing key shortfall – report

With experts predicting that Britain faces a retirement crunch point within the next 20 years, we reveal those most likely to be affected and the key risks to your savings.

The UK is heading for a pensions crisis within the next two decades, with 2.7 million people retiring on less than they need, new figures have revealed.

According to data from Phoenix Insights reported in This is Money, 59% of savers with defined contribution pensions – based on what they put in and not their final salary – will not have enough to live on in retirement.

These individuals are part of what has been identified as a “lost generation” of savers.

Now in middle-age, they did not benefit from the more lucrative defined benefit schemes available to their predecessors.

As a double blow, they also missed out on the lifetime of auto-enrolment available to younger workers.

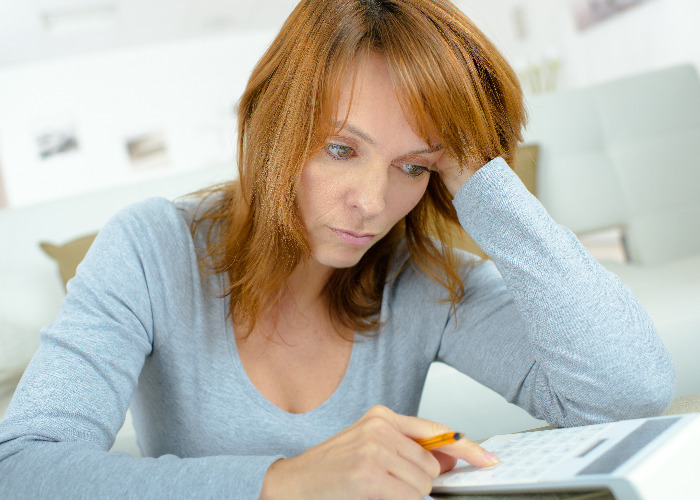

Who will be hit?

According to This is Money, those likely to be most affected are women born in the 1970s and earning below £80,000 – 50% of them under £20,000.

Many of these "undersavers" will leave the workforce between 2040 and 2044, which Phoenix has identified as a critical juncture for the industry.

The research also found that most of these women expect to retire between the ages of 66 and 70.

Commenting on the findings, Patrick Thomson, head of research analysis and policy at Phoenix Insights, said: “The analysis paints a bleak picture of future retirement incomes.

“We are already reaching the stage where the majority of people with a defined contribution pension will enter retirement with either less than they expect, or less than they need in terms of a minimum living standard.

"This situation is set to worsen over time and peak in the next 20 years.

"There is an urgent need to address undersaving to better support people to achieve financial security later in life."

3 pensioner perks at risk in the Budget

A raid on tax-free lump sums?

Unsurprisingly, the research puts the spotlight on the upcoming Budget and what Chancellor Rachel Reeves has in store for pensions.

While the Government’s plans have yet to be confirmed, there are fears that Labour may target the tax-free lump sum on pension withdrawals.

At present, people can take up to 25% of their personal or workplace pension as a tax-free lump sum when they reach the age of 55 – rising to 57 in 2028.

The current system allows pensioners to take up to £286,275 before they start paying tax.

That said, think tank the Institute for Fiscal Studies (IFS) recently urged the Government to place a £100,000 cap on the amount people can claim before they start paying tax.

A flat rate of relief

Alarmingly, this lost generation could also be hit by the Chancellor’s predicted raid on pensions tax relief.

Under current rules, the amount of relief savers receive when paying into a pension is determined by their Income Tax bracket.

For Basic Rate taxpayers, contributions are topped up by 20%, meaning that a £100 contribution costs £80. Higher Rate taxpayers get 40% relief and Additional Rate taxpayers receive 45%.

In 2016, then-backbencher Rachel Reeves expressed support for a flat rate of 33% relief for all savers.

According to data from think tank, the Fabian Society, a flat rate could raise £10 billion a year for the Government.

Why even retirees with “gold-plated” pensions are worse off

Have your say

Are you a mid-life woman concerned about your savings income? Or perhaps you belong to a different demographic and feel just as concerned.

We’d love to hear your comments.

Comments

Be the first to comment

Do you want to comment on this article? You need to be signed in for this feature