Best and worst banks: how customers rate their service

We reveal the banks that are most (and least) likely to be recommended by their customers. Does yours make the list?

If you want to know which banks are worth joining and the ones you should avoid, it's worth listening to what customers who actually bank with each brand have to say.

Various institutions will regularly poll the public to understand how happy they are with their bank.

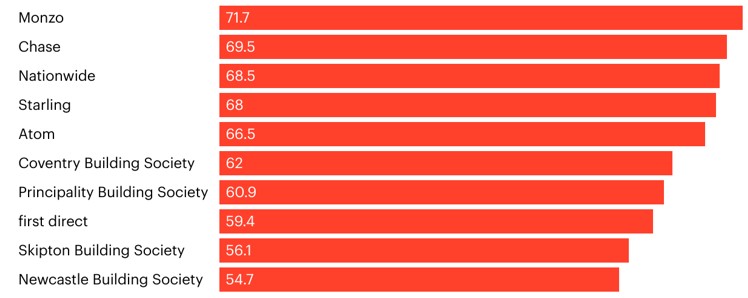

The latest such survey comes from Yougov, which revealed that Monzo customers were the most likely to say they were satisfied.

It was followed by Chase, Nationwide and Starling Bank.

It's interesting to note that smaller 'challenger' banks and banking apps rank so highly, taking three of the top four spots.

Because these businesses often have fewer overheads, they can make the most of modern technology to deliver services that customers really value.

Monzo and Starling, in particular, have led the way with app-based functionality and perks such as fee-free spending abroad.

Perhaps the standout result of the Yougov data is First Direct, a perennial winner in customer satisfaction surveys, only finishing eighth.

You can see the top 10 banks and building societies below, ranked by net satisfaction score (number of people satisfied with their bank minus those dissatisfied).

Banks with the highest satisfaction levels

Source: Yougov

Frustratingly, Yougov won't reveal the banks that fared worst in their survey.

To get a more detailed view of the banks that did well and, importantly, those that didn't, we need to turn to the Competition and Markets Authority (CMA).

Its latest data, conducted with research firm Ipsos, looks at personal current account holders’ experiences between July 2023 and June 2024.

Customers were asked about online and mobile banking, branch experiences, overdrafts, and, crucially, how likely they were to recommend their bank to friends, family, or business contacts.

Banks we're most & least happy with

|

Rank |

Bank |

Recommendation rate |

|---|---|---|

|

1 |

Monzo |

82% |

|

2 |

Chase |

78% |

|

3 |

Starling |

78% |

|

4 |

First Direct |

75% |

|

5 |

Nationwide |

70% |

|

6= |

Lloyds Bank |

66% |

|

6= |

Halifax |

66% |

|

8= |

Bank of Scotland |

63% |

|

8= |

Barclays Bank |

63% |

|

10 |

Metro Bank |

61% |

|

11 |

Santander |

58% |

|

12 |

HSBC UK |

57% |

|

13 |

NatWest |

56% |

|

14 |

TSB |

54% |

|

15 |

The Co-operative Bank |

51% |

|

16 |

Virgin Money |

50% |

|

17 |

Royal Bank of Scotland |

49% |

Source: Ipsos

The worst offenders

As you can see from the table above, traditional high-street banks struggled in the ratings.

According to the data, The Co-operative Bank, Virgin Money and Royal Bank of Scotland ranked lowest for customer satisfaction.

Certainly, the big banks dominated the bottom half of the table, suggesting they have a long way to go in terms of keeping their customers happy.

Online and mobile accounts

With banking increasingly moving into the digital space, the researchers also asked about users’ experiences of online finance.

Here is what they discovered.

|

Rank |

Bank |

Recommendation rate |

|

1 |

Monzo |

87% |

|

2 |

Starling |

84% |

|

3 |

Chase |

83% |

|

4 |

Halifax |

79% |

|

5= |

First Direct |

78% |

|

5= |

Bank of Scotland |

78% |

|

7= |

Lloyds Bank |

77% |

|

7= |

Nationwide |

77% |

|

9 |

Barclays |

76% |

|

10 |

HSBC UK |

72% |

|

11 |

Metro Bank |

71% |

|

12 |

Santander |

70% |

|

13 |

NatWest |

69% |

|

14 |

Royal Bank of Scotland |

67% |

|

15 |

TSB |

66% |

|

16 |

Virgin Money |

59% |

|

17 |

The Co-operative Bank |

56% |

Source: Ipsos

Given the category, it’s perhaps unsurprising that banks without a high-street presence topped the tables.

As these institutions have fewer overheads, they can focus on lowering rates and making their online services as attractive as possible.

Overdraft services

Amid the ongoing cost-of-living crisis, it’s unsurprising that the experts also looked at the cost of borrowing.

According to the findings, Monzo, Starling and Lloyds were the three highest rated banks, with scores of 78%, 75% and 72% respectively.

At the other end of the scale, Royal Bank of Scotland and NatWest had ratings of just 49%.

Cheap and free overdrafts: best current accounts for those who go overdrawn

Have your say

What do you make of these findings? And how do you feel about your current bank?

Do you agree that app-only banks are the future or perhaps you’d rather do your banking from a branch?

Let us know in the comments below.

Get great customer service and earn 3.25% on your balance with a Starling Bank current account (affiliate link)

*This article contains affiliate links, which means we may receive a commission on any sales of products or services we write about, but it won't affect the price you're offered. This article was written completely independently.

Want more stories like this? Head over to the loveMONEY homepage, follow us on Twitter or Facebook or sign up for our newsletter and let us send the news to you!

Comments

Be the first to comment

Do you want to comment on this article? You need to be signed in for this feature